What is a Blockchain?

A blockchain is a decentralized ledger that records all transactions that take place across a peer-to-peer network. Transactions are time-stamped and aggregated into back-linked blocks that are encrypted and structured into chains. These blocks include immutable transaction data that is regarded as trustworthy and secure. All blockchain network users can witness any transaction ever made by anyone on the network thanks to blockchain technology.

The following are the three most prevalent blockchain network architectures:

Networks that function with untrusted members, such as Bitcoin and Ethereum, use a public architecture with permissionless access.

Permissioned access to public architecture — Ripple, for example, is a network that only deals with trusted users.

Permissioned access to a private architecture — Bankchain and FiberChain are two examples of networks that are only accessible to trustworthy members of a particular group

According to Forrester, a permissioned blockchain is a safer and wiser choice than a permissionless blockchain, which poses too many compliance difficulties.

Main Blockchain Elements

Network User: An individual having a token wallet, a digital signature, and two keys- public and private

Nodes: Computers on the peer-to-peer network that form the blockchain's infrastructure

Transactions: A transaction includes the public key of the receiver, information about the transaction's value, and the sender's digital signature

Authentication: Nodes authenticate transactions sent by a user

Blocks: Blocks are created by validator nodes that select pending transactions

Blockchain: Validated blocks are linked to each other with a unique hash- a fingerprint of the data in the previous block

Companies interested in experimenting with blockchain technology can create their own private blockchain or use and partially alter a public blockchain network to meet their specific needs. In any event, they will be able to take advantage of the blockchain's main security features.

The Fundamentals of Blockchain Security

By definition, a blockchain is distributed and replicable. It is based on participant consensus and the most recent cryptographic advances. As a result, blockchain-based solutions are more secure than non-blockchain systems against cyberattacks.

The security of blockchain technology is based on three key factors:

Confidentiality— The blockchain has a lot of features that help users keep their identities hidden. The only thing that connects a user to their data is their user key. These keys, on the other hand, are simple to mask. To maximize users' confidentiality, several networks employ non-interactive zero-knowledge proofs (zk-SNARK, zk-STARK, and so on). As a result, a blockchain allows users to maintain unprecedented levels of anonymity while being open and affording rich options for transaction tracking.

Data integrity— Blockchains are ledgers in which each block uses cryptographic hash algorithms to link to neighboring blocks. As a result, once a transaction has been recorded on the blockchain, it cannot be changed or removed. Any modifications to previously recorded data are treated as new transactions.

Availability– A high number of nodes enables blockchain resiliency, even if some are unavailable. Because each node in the network has a copy of the distributed ledger, even if one node is compromised, other peers can still access the correct blockchain.

Organizations are turning to blockchain-based solutions to bring all of these qualities to their software products. The technological intricacy of blockchain technology, on the other hand, raises certain doubts about its application and long-term viability.

Using the Blockchain for Cybersecurity: Pros and Cons

While the blockchain has a lot of potential as a cybersecurity solution, it also comes with a lot of risks. Let's take a deeper look at the major limitations of blockchain technology that you should consider before opting to use it to improve the security of your solution:

Scalability issues– Distinct blockchain networks have different restrictions, such as block size and transaction throughput per second. As a result, you should investigate the scalability of any blockchain platform you want to employ as the foundation for your solution.

The current restrictions for Bitcoin are 1 MB of data and up to 7 Transactions Per Second (TPS). Block creation on the Ethereum network is limited to 7 to 15 TPS. Other networks, on the other hand, claim to have far more transaction capacity. For example, Ontology claims to be able to reach 4,000 to 12,000 TPS depending on the environment, whereas the Futurepia network has been tested to exceed 300,000 TPS.

Reliance on private keys— Blockchains relies on the use of private keys, which are long sequences of random integers created automatically by a wallet. In contrast to user passwords, private keys are used to communicate with the blockchain and cannot be recovered. If a user's private key is lost, all data encrypted with it is very certainly lost forever.

Adaptability challenges— Despite the fact that blockchain technology may be used in practically every industry, businesses may have difficulty incorporating it. It's difficult to use this technology in supply chain systems, for example, because re-implementing supply chain logic using a blockchain could take a long time. Companies should examine this before deploying blockchain technology because blockchain applications may need the total replacement of old systems.

Risk of cyberattacks— Although blockchain technology minimizes the danger of hostile interference, it is not a cure-all for all cyber threats. Node connectivity (the eclipse attack), consensus procedures (the 51 percent assault), and code vulnerabilities are all flaws in the blockchain. If attackers are successful in exploiting any of these flaws, the entire system's security may be jeopardized.

High operation and customization costs— A blockchain system necessitates a lot of computational power and storage space. In comparison to existing non-blockchain systems, this could result in greater marginal costs.

Blockchain literacy— Despite the growing popularity of blockchain technologies, qualified blockchain developers and cryptography experts are still in short supply. Blockchain development necessitates a diverse set of abilities as well as a thorough understanding of various technologies, programming languages, and tools.

Lack of governance— Globally, the operation and usage of blockchain technology in general, and distributed ledgers, in particular, are unregulated. Many nations, notably Malta and the United States, have already enacted or are in the process of enacting cryptocurrency rules. Several states in the United States have also enacted legislation governing the legal and commercial usage of blockchains and smart contracts.

These are the key blockchain disadvantages to consider when determining whether or not to use this technology to improve your product's cybersecurity. However, based on the business you work in and the additional duties you want to accomplish using the blockchain, the final scope of possible drawbacks will vary.

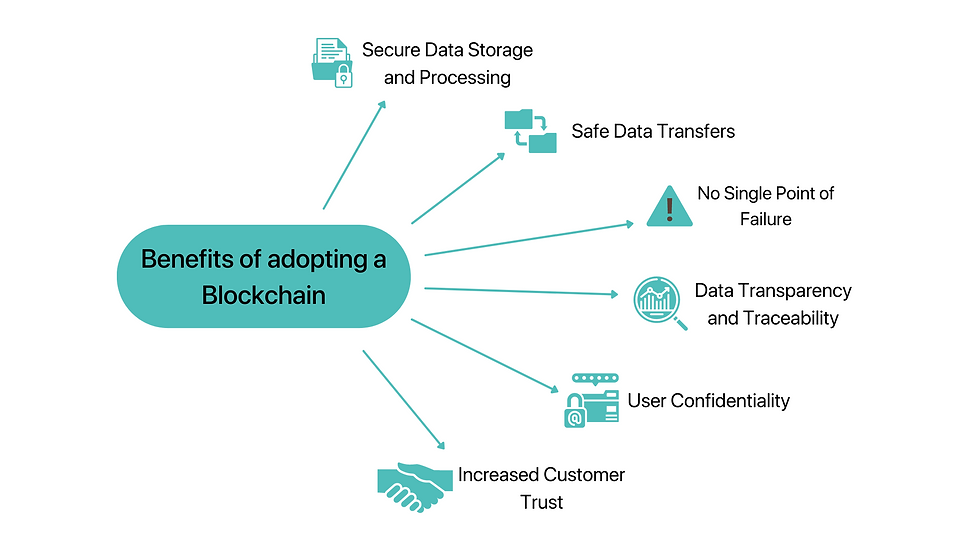

Let's look at some of the main benefits of adopting a blockchain for cybersecurity:

Secure data storage and processing— Any modification recorded on the blockchain is transparent and non-removable, and blockchain records are immutable. As a result, data saved on a blockchain is more secure than data maintained on traditional digital or physical records.

Safe data transfers— The blockchain allows for quick and secure data and financial transactions. Smart contracts, for example, allow for the automatic implementation of agreements between several parties.

No single point of failure— Permissionless blockchain technologies are more resilient than traditional systems because they are decentralized. The functioning or security of the blockchain will not be harmed if a single node is compromised. This means that even if the system is subjected to DDoS attacks, the system will continue to function normally as a result of numerous copies of the ledger. Private blockchains, on the other hand, cannot provide you with this benefit.

Data transparency and traceability— All blockchain transactions are digitally signed and time-stamped, allowing network users to readily trace transaction history and follow accounts at any point in time. This capability also helps a corporation to have accurate asset or product distribution information.

User confidentiality— Because users are authenticated using public-key cryptography, the secrecy of blockchain network participants is high. Some blockchain-based firms, on the other hand, take this technology a step further and improve it. Guard time, for example, created a Keyless Signature Infrastructure (KSI) that allows users to check the validity of their signatures without revealing their keys.

Increased customer trust— A blockchain can help firms achieve customer trust by providing data privacy and transparency. Furthermore, in many of today's blockchain networks, data owners can have complete control over their personal information and select who and when can access it.

Let's look at which industries stand to gain the most from using blockchain technology to improve the security of their products.

Sectors Benefiting from Blockchains for Cybersecurity

The blockchain, by its very nature, presents potential cybersecurity solutions to startups and businesses in a variety of areas. The following are some of the industries that could benefit the most from blockchain-based cybersecurity:

Finance:

The most significant value of a blockchain in the financial sector is its data immutability and transaction transparency. Keeping traditional digital or physical records is less transparent and safe than storing transactions on the blockchain. To preserve the security of consumer information, several banking institutions, like ING Group, use blockchains and, in particular, zero-knowledge range proof solutions. To protect customer data, Q2, a virtual banking platform, employs blockchain and machine learning.

Many blockchain networks include smart contracts, which allow for the automatic execution of agreements between many parties if all of the conditions are met. Pledge agreements and deposits are common instances of such agreements.

Healthcare:

Healthcare firms, like the financial sector, may profit substantially from the use of blockchains for securely storing and efficiently sharing medical data. BurstIQ, for example, is a blockchain-based technology that enables healthcare organizations to securely store patient data and exchange it in real-time between departments and institutions.

A blockchain can also be used to provide secure messaging systems for quick and easy communication between patients and institutions in administrative and non-urgent medical matters.

Real Estate:

Blockchains are now used by real estate platforms to solve two primary problems: assuring secure data storage and automating important operations like authenticating property ownership and transferring cash. A blockchain permits property ownership and payment history to be kept immutable and transparent. This technology is used by StreetWire and ShelterZoom to make data administration easier for real estate companies.

A blockchain also provides stability and automation, both of which are critical for real estate enterprises to operate successfully. Smart contracts are used by companies like SMARTRealy and Propy to sell, buy, and rent real estate. Smart contracts ensure that agreements between multiple parties be executed quickly, securely, and completely automatically.

Supply Chain:

Blockchains are being used by global corporations such as Walmart, BMW, and FedEx to improve data security and operational transparency. To facilitate the examination of a supply chain's efficiency and operations, a blockchain can contain tamper-proof records of all activities, transactions, and freight data.

Asset authentication can also be done using blockchain systems. Organizations are shifting their focus away from centralized authorities and toward trust models based on algorithms, according to Gartner. The blockchain is a great illustration of this type of model.

Governance:

Many government activities, including tax collecting, information governance, elections, and so on, can benefit from blockchain technology. Catena, a blockchain-based platform for assessing government spending, is used by the Canadian government.

A blockchain can be used to speed up vote counting and assure the accuracy of election results in the case of elections. Tampering with electronic voting on a blockchain becomes nearly impossible due to the immutability of all data records. Maintaining the anonymity of a voter's choice while authenticating their identity, on the other hand, maybe difficult.

As you can see, blockchains may be used in a variety of industries to increase the security of data, financial transactions, and communication.

Conclusion

Due to dependable data encryption technologies, data integrity, network resilience, and scalability, the blockchain provides a wealth of opportunities for maintaining a high degree of data security. As a result, firms in practically every industry can benefit from migrating from a traditional system to a blockchain-based one.

When adopting a blockchain to improve the cybersecurity of their products, however, enterprises should be prepared to cope with several downsides and challenges, just as they should with any revolutionary solution. The use of private keys, adaptation concerns, and a lack of competence are all major obstacles.

For more information visit us on: www.nexixsecuritylabs.com

To schedule an audit you can contact us at: contact@nexixsecuritylabs.com

Your Security | Our Concern

Comments